Whose Housing Recovery?

High-finance investors are snapping up tens of thousands of foreclosed homes for rental income and speculation.

The business press has been reporting a "recovery" of the U.S. housing market for over a year now, as the average prices of single-family homes rise across the country. Implied in these stories is the return of a healthy real-estate market, in which the average American family has the resources--in terms of income, savings, and access to credit--to purchase its own slice of the American dream.

The housing recovery we are seeing right now, however, is anything but indicative of broader gains--increased wages, falling unemployment, or renewed access to credit for consumers--being shared across the economy. The biggest buyers of single-family homes today are not new owner-occupants, but investors. While most of these investors are so-called "mom-and-pop" buyers who own an extra rental house or two in their hometowns, large private investors are also increasingly buying up homes.

These investors are especially focusing on foreclosed properties in the "sun" and "sand" belts--from Florida and Georgia to Arizona, Nevada, and California. Private-equity firms, investment banks, and other high-finance investors are gobbling up housing stocks in these markets by the tens of thousands of units. They have taken to calling single-family rental homes a "new asset class," alongside corporate debt, government bonds, currencies, and financial derivatives.

From Owners to Renters

Under the so-called housing recovery, the foreclosed homeowner is being relegated to the status of renter. Increasingly, the new renters' role will be to pay their new high-finance landlords for shelter, all in order to secure big returns for the millionaire clients and institutional partners who are backing foreclosure purchases with billions of dollars.

After decades of hovering around 63-65%, the percentage of Americans who own their homes shot upward starting in 1995. The growth of the subprime-mortgage business created millions of new homeowners, and by 2005 homeownership in the United States peaked at a record 69%. Predatory lending by banks--especially subprime loans whose low "teaser" interest rates ballooned after a couple of years--along with stagnant wages and mounting non-mortgage debt, stretched the finances of many homeowners. When the financial crisis of 2008, centered on securitized mortgage debt, crashed the global economy, a cascade of foreclosures began. Millions lost their homes along with their jobs and retirement savings. This was reflected in a roughly 3-percentage-point drop in the national homeownership rate--from 69% to 66%, according to figures from the Federal Reserve Bank of St. Louis. An influential report by the John Burns Real Estate consulting firm, however, shows that counting homeowners who are now more than 90 days late on their mortgage payments--and are likely to end up foreclosed--the real decline in homeownership is likely to be 7 percentage points. That would take the homeownership rate down to about 62%, substantially lower than before the post-1995 surge.

Homeownership is overly romanticized in American culture, and is not necessarily an intrinsically good thing. (See Howard Karger, The Homeownership Myth, Dollars & Sense, March/April 2007.) In the United States, however, single-family homes have historically provided a place for families to safely invest and build wealth. In recent decades, rising home prices helped finance college educations and health care for working- and middle-class families, even as wages stagnated.

Being a renter also tends to cost more. Although the mortgage-to-rent ratio (the measure of how much it costs to finance the purchase of a home versus renting one) varies depending on many factors, it is usually true that mortgage payments are well below the rental costs for similar housing. This is especially true now that mortgage rates have dropped to about 3.5% even as rents have risen. In other words, being forced to rent because of a foreclosure means, for millions of Americans, paying a higher percentage of their incomes for housing (and, often, living in smaller quarters).

The millions of foreclosures since 2007 represent a massive upward redistribution of wealth. Millions of families have lost or are on the verge of losing their single largest asset, which has served as a source of security and access to credit. Neither they nor those who would normally be likely first-home buyers are able to buy. Those who are buying are largely investors looking for bargain real estate on which they can turn a profit, both in rents and through eventual sale, after home prices have risen.

Enter the Federal Government

The federal government has lent little assistance to homeowners in danger of foreclosure, or to renters seeking to purchase a first home. Instead it has focused its monetary and policy powers on the well-being of the banks at the center of the financial system. The sum of taxpayer dollars used to bail out the largest banks, which hold millions of mortgage loans, dwarfs the mortgage relief from settlements reached between the federal government and the nations largest lenders. For example, Citibank received $50 billion in Troubled Asset Relief Program (TARP) payments in 2008, and $426 billion more in other forms of government assistance, according to the Congressional Oversight Panel that tracked Treasury's spending of TARP funds. While Citibank has since repaid the federal government, this public assistance allowed the company to survive, thereby maintaining the incomes and wealth of major shareholders and executives. Under the mortgage-servicer settlement agreed to last year, however, Citigroup is only being made to provide $1.8 billion in relief to borrowers who were defrauded by the bank during the financial crisis.

What's more, it was the combination of the economic collapse in 2008, and more recent interventions by the U.S. Federal Reserve (The Fed) and federal housing agencies, that sowed the seeds of opportunity for powerful investors to purchase homes at historically low prices. The federal government's key housing-market intervention has been a program of purchasing "agency mortgage-backed securities," under a third round of "quantitative easing" (or "QE3"). Mortgage-backed securities (MBSs) are claims on payments from mortgage loans. Only MBSs associated with fixed-rate mortgages backed by agencies like Fannie Mae and Freddie Mac are being purchased under the program. Under QE3, the Federal Reserve is buying upwards of $40 billion in mortgage debt each month. These huge purchases drive up the prices of housing bonds, thereby lowering the yields (interest rates) on the bonds. In theory, this should create conditions for renewed bank lending to homebuyers. As it becomes more expensive to purchase existing mortgage securities, and the returns on these securities decrease, capital should flow into new home loans. But without recovered employment, incomes, and savings, many U.S. households are in no position to make such a big purchase. Worsening this situation is the fact that loan standards have been tightened by all of the major mortgage lenders, making it much more difficult for those with little savings or low incomes to purchase a home.

Big investors are quickly taking advantage of the housing market's peculiar condition. The lack of competition from prospective owner-occupiers makes it easy for them to make bulk purchases of housing. The growing number of renters nationwide means there are people ready to pay to live in the newly purchased homes. And the Fed's recent intervention has led investors to expect home-price increases in the future, potentially creating another source of profit.

Meanwhile, in the Mainstream Business Press...

Meanwhile, in the Mainstream Business Press...

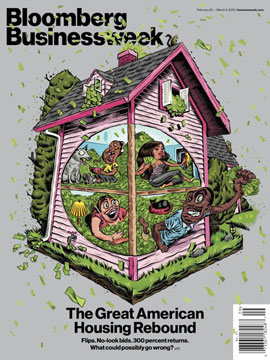

The title of Ryan Chittum's Feb. 28 Columbia Journalism Review blog post summed up what was wrong with the cover of Bloomberg Businessweek we are parodying in this issue's cover: A BusinessWeek cover crosses a line: Minorities as greedy grotesqueries fueling a new housing bubble. Chittum nicely situated the cover in the trend at the weekly, since it was taken over by Bloomberg, toward deliberately "edgy" cover designs.

As Chittum points out, besides its grotesque racial caricatures, the cover reinforces the right's thoroughly discredited "blame-minority-borrowers" narrative about the origins of the last housing bubble. While in fact "minority borrowers were disproportionately victimized by the bubble, Businessweek has them on the cover bathing in housing-ATM cash, implying that they're going to create another bubble." Yet the cover article itself doesn't reinforce that narrative at all. Instead, it reports on the resurging housing market in Phoenix, Ariz., with a focus on house-flipping and a brief mention of big-money investors.

Businessweek editor Josh Tyrangiel issued this non-apology via POLITICO: "Our cover illustration last week got strong reactions, which we regret. Our intention was not to incite or offend. If we had to do it over again we'd do it differently." --Eds.

The Return of the Financiers

Not all investors waited for the federal government's recent efforts to pump up home prices. One company, Waypoint Homes of Oakland, Calif., began to buy up thousands of foreclosed houses in the Bay Area and Los Angeles as early as 2008. Since 2012, the firm has used a commitment of $400 million to $1 billion from GI Partners, a California private-equity group, to expand nationally. Waypoint now owns upwards of 4,000 homes, mostly in California, Arizona, Illinois, Georgia, and Florida, and is buying dozens more every week. Citibank has extended Waypoint $250 million in credit for its purchases, just one indication of the serious money this industry is now attracting.

In August 2010, the Federal Housing Finance Administration (FHFA) announced that it was seeking input from the real-estate investment industry on how to deal with foreclosed homes sitting on the balance sheets of the government-sponsored loan agencies, Fannie Mae and Freddie Mac. The industry responded with a slew of proposals, all centered on allowing private investors to buy up the government's inventory of over 90,000 foreclosed homes. As a result, the FHFA decided to set up a "pilot program" to sell off its foreclosed housing inventory, and invited investors to submit bids.

In September 2012, the FHFA announced the first of its winning bidders. Pacifica Companies, LLC, took control of 700 homes in Florida. Shortly thereafter, the New York-based Cogsville Group, LLC, took control of 94 homes in Chicago, and the Los Angeles-based Colony Capital took over 970 houses in California, Nevada, and Arizona.

These transactions, however, were small potatoes compared to what has been building in the private housing market, where there are millions of foreclosed homes on the books of banks and mortgage-lending companies. Investor buyouts of entire stocks of regional foreclosed housing inventories began in earnest in 2011 and have shown little sign of slowing.

According to numerous press reports, the Blackstone private-equity fund has been the hungriest purchaser of foreclosed homes, having bought upwards of 16,000 houses across the country. A January 2013 report in Bloomberg News described Blackstone as "rushing" to spend the $2.5 billion the firm has allotted toward foreclosure buyouts. The second largest foreclosure-to-rental mill is Carrington Holding Company, a California-based firm that began as a mortgage servicer during the housing boom of the 2000s, but which has morphed into a private-equity landlord. Carrington reportedly owns 4,500 homes today in Chicago, Miami, Phoenix, and Las Vegas. American Homes 4 Rent, a company set up by Wayne Hughes, the billionaire owner of Public Storage Properties, is chasing Waypoint, Colony, Carrington, and Blackstone, using a $400 million commitment from the state-controlled Alaska Permanent Fund.

Silver Bay Realty, one of the few public corporations to enter the foreclosure-to-rental business, described its business plan in a December 2012 prospectus. "As the housing market recovers and the cost of residential real estate increases, so should the underlying value of our assets," the company's management explained. "We believe that rental rates will also increase in such a recovery due to the strong correlation between home prices and rents. This trend also leads us to believe that the single-family residential asset class will serve as a natural hedge to inflation. As a result, we believe we are well positioned for the current economic environment and for a housing market recovery."

There are perhaps as many as fifteen or twenty other investment firms focused on buying up foreclosed homes and transforming them into assets from which value can be extracted by either rental or sale. No one actually knows how many companies are in this nascent industry, how many homes they have bought, or how much money that have spent. A February 2013 Barclays research report estimates that just over 42,000 foreclosed homes, mostly in California, Arizona, Georgia, Florida, Nevada, and Illinois, have been taken over by private investors. Others have put the figure lower or higher by tens of thousands. What is clear is that the industry is growing quickly.

The $60 Billion Question

More than 40,000 homes is a lot, but given that approximately 4.1 million single-family homes traded hands last year, it would mean that the rise of the private-equity landlord is still a relatively small phenomenon--about 1% of all sales in a market still dominated by owner-occupiers and mom-and-pop investors. The rapid growth of the foreclosure-to-rental mills, however, means that institutional investors could soon overtake other buyers, and dominate particular regional markets. That's what money managers at some of the biggest investment banks are hoping at least.

Analysts at Morgan Stanley call the industry's growth potential the "$60 billion question." Keeping in mind that only about $5 billion has been spent by private equity to buy out foreclosed homes to date, this would mean the U.S. housing market could be poised to see a more than ten-fold increase in foreclosure-to-rental conversions. The analysts at Barclays are even more bullish, saying they think this could grow into a $100 to $200 billion dollar market, encompassing as many as 1.3 million single-family homes.

What this means for many communities, especially residential neighborhoods in Arizona, California, Florida, Georgia, and other hot spots of investor activity, is that home ownership will become an increasingly difficult goal to attain as big-finance investors monopolize the stock of available housing in search of big profits. It also means that as the Fed continues its mortgage-bond buying spree to push up housing values, the parties best poised to reap these gains in equity will be Wall Street investors, rather than owner-occupiers.